Insurers have significantly tightened their underwriting over the past 12 – 18 months, and the level of data required before quoting has increased acrosss the board.

What’s changed?

Insurers are now scrutinising risk information far more closely than they used to. Where a brief overview may have been enough in the past, underwriters today want specifics: detailed claims histories, updated asset values, current risk management practices, workforce numbers, and revenue breakdowns. We are essentially asking for the works.

It’s not about being difficult. It’s about insurers protecting their books in a tougher market.

And here’s the reality: incomplete or vague information leads to higher premiums, coverage restrictions, or declined quotes.

Why we’re asking (again)

We know it can feel repetitive. You provided this information last year, and your business hasn’t changed significantly. Why do we need it all over again?

Because insurers treat every renewal as a fresh underwriting exercise. They’re reassessing your risk profile based on current information, not last year’s data. If we don’t provide comprehensive, accurate details upfront, we lose negotiation power, and potentially you may lose more as a result.

What good information gets you:

Sharper pricing – Underwriters price what they understand. The clearer the picture, the tighter the premium.

Broader coverage – Detailed risk information helps us argue for better terms, higher limits, and fewer exclusions.

Faster turnaround – Complete submissions avoid the back-and-forth that delays quotes and eats into your renewal timeline.

More options – Insurers are more willing to quote and complete when they have confidence in the information.

Our commitment to you

We are not asking for details to tick boxes. We’re asking to secure the best possible outcome for your business. Every data point you provide gives us leverage to negotiate on your behalf, and in this market, that leverage matters.

We also get that you’re busy. If there’s a way we can make the renewal process easier by pre-filling forms, scheduling a quick call instead of lengthy emails, or consolidating requests, please let us know. We’re here to make this work for you, not add to your workload.

What this means for your business

The more detail we have, the harder we can push for competitive terms. It might feel like extra effort now, but it translates directly into better cover and better value when renewal time comes.

As always, if you’ve got questions about what we’re asking for (or why), we’re happy to walk you through it.

For Martin Turner, recruitment has never been just about filling roles. It’s about helping people find opportunity, guiding careers, and building connections that can genuinely change lives.

As one of the founders of TTG, Martin has spent more than three decades helping businesses find the right people and supporting individuals to step into roles where they can thrive.

Along the way, he’s navigated economic downturns, industry challenges, and delivered some of Australia’s largest recruitment projects.

His journey into business wasn’t part of a grand plan. After building a career in human resources and recruitment consultancy, Martin and a group of colleagues saw an opportunity to do things differently.

In 1991, four founders took a leap of faith and launched TTG. More than 30 years later, that decision has grown into a trusted recruitment business that has helped thousands of people and organisations find the right fit.

Riding out the storms

Like many long-standing businesses, TTG has weathered its share of challenges.

From the Global Financial Crisis to COVID-19, there were times when hiring slowed, projects paused, and confidence in the market dropped. As Martin explains, recruitment is closely linked to business activity. When clients slow down, hiring slows too. When confidence returns, recruitment picks up again.

One constant challenge throughout the years has been cash flow, particularly when working with large organisations that come with complex processes and longer payment cycles.

Despite this, Martin credits the team’s resilience and adaptability for the business’s continued growth.

A project close to home

While TTG has partnered with major organisations across Australia, one project stands out.

When Brisbane’s public transport network changed from Go Card to contactless payments, Translink asked TTG to help with the rollout. The team was tasked with recruiting 140 employees for a large customer engagement campaign.

For a relatively small team, it was a major undertaking. They interviewed hundreds of candidates, onboarded successful applicants, coordinated training programs, and provided ongoing performance management throughout the project.

What began as a single recruitment assignment grew into a trusted three-year partnership, a clear reflection of the team’s ability to deliver great results.

Helping people find their place

While large projects are rewarding, what keeps Martin motivated is simple: helping people find work they truly enjoy.

Many young professionals come to him unsure of what they want to do. Sometimes, they only know what they don’t want.

Martin enjoys helping them discover opportunities they may not have thought about and guiding them towards careers that suit their skills, goals, and personality.

For him, helping people build a career they love is the most rewarding part of the job.

Lessons learned along the way

After more than 30 years in business, Martin has learned plenty but one lesson stands out: don’t do it alone.

Building strong relationships with mentors, advisers, and trusted partners can make all the difference when challenges arise.

He also believes in the importance of delegation; surrounding yourself with capable people and trusting them to do what they do best, so he can focus on growing the business.

Life beyond recruitment

Outside of work, Martin has discovered a new passion: winemaking.

What started as a hobby is slowly growing into a business. He plans to obtain a wine licence and one day sell his own wines, with the profits going towards charitable causes that are close to his heart.

When he’s not in the vineyard, you’ll likely find him watching rugby on TV. A proud Welsh rugby fan, he rarely misses a match.

After decades spent helping others build their careers, Martin continues to explore new passions of his own. And if his journey has shown anything, it’s that great opportunities often begin with a willingness to take a chance.

One of our landscaping clients faced a costly setback when the incorrect fuel was accidentally added to their work vehicle, causing significant damage.

With the vehicle off the road, their ability to operate and generate income was immediately affected.

At first, the insurer approved the claim. However, four weeks after lodgement with no additional information provided, the insurer reversed their decision.

They advised that they misread the policy and that the claim, including both repairs and downtime would not be covered.

This sudden change left our client feeling confused and under pressure. The business had already been disrupted and the claim outcome had shifted.

Our role as your insurance claim support

This is where our team stepped in to provide them with insurance claim support.

Our insurance claim support team reviewed the situation and challenged the insurer’s decision. We highlighted a few key points:

The client had been open and honest from the start

The insurer had already indicated the claim would be covered

The delay in changing the decision put the client at a disadvantage

The insurer finally agreed to cover the repair. However, they still declined the downtime insurance claim.

We didn’t stop there. Given that downtime cover had been clearly discussed earlier with the insurer, we continued to push the matter further.

We escalated the case to a Dispute Resolution Officer. We also continued negotiations over several months to seek a fair outcome.

The outcome

After persistent follow-up and strong advocacy from our insurance claim support team, the insurer agreed to cover both the repair and the downtime claim.

This result made a real difference to our client. It helped them recover financially and get their business moving again.

Key takeaways:

Insurance claims do not always go smoothly. Decisions can change, and the process can feel overwhelming.

This is where having a broker can make a real difference.

Without insurance claim support, many business owners do not have the time or energy to challenge claim decisions or navigate disputes. Some may even accept an outcome that is not fair.

When you work with a broker, we handle the claim process for you. We advocate on your behalf as your insurance claim support and deal with the insurer directly.

You can focus on your business, knowing you have someone in your corner when it matters most. Learn more about our claim services. here.

Running a business comes with risks. Accidents, property damage, and legal claims can happen at any time, even when you’ve done nothing wrong. That’s why liability insurance is so important.

At its core, liability insurance is triggered when a claim of negligence is made against you or your business. Even if you did nothing wrong, defending yourself in court can be very expensive. Liability insurance for businesses helps cover both the costs of being found negligent and the significant expenses involved in defending a claim.

Liability insurance protects your business if someone says you caused them financial loss, injury, or property damage. It covers both any compensation you might owe and the legal costs of defending yourself.

This coverage is essential because defending a claim, even if you did nothing wrong, can cost tens or hundreds of thousands of dollars. Liability insurance makes sure you don’t have to pay these costs yourself.

What does Liability Insurance cover?

Liability insurance is meant to protect you from:

Claims of negligence – if someone alleges your actions (or failure to act) caused them financial loss, injury, or property damage.

Legal defence costs – including lawyer’s fees, court filing costs, expert witnesses, and settlement negotiations.

Damages or compensation – if you are found liable.

This applies to a wide range of scenarios, from a customer slipping on your premises to damage caused to someone else’s property while on a job site.

What is the trigger? Negligence

The most common trigger for liability claims is an allegation of negligence. Negligence doesn’t mean you intended to cause harm, it could simply mean someone believes you failed to take “reasonable care.”

For example, a cafe owner might be sued if a customer slips on a wet floor and becomes injured. Another scenario could be a tradesperson being sued if their work is alleged to have caused property damage.

How does it protect your business?

You don’t need to lose a case to lose money. Even if you haven’t been negligent, defending yourself in court can be extremely expensive. Lawyers’ fees, expert reports, and court appearances can quickly add up to tens or hundreds of thousands of dollars.

Liability insurance covers these defence costs, so your business can keep running while the case is ongoing. Without it, you might have to pay out of pocket, which could be a financial blow many businesses can’t handle.

Do you need liability insurance? A broker would know

Liability insurance is not just protection for when mistakes happen. It’s protection against the rising costs of legal disputes and claims, even when you’ve done everything right.

Understanding the level of protection you need can be complex, which is why speaking with an experienced broker can make all the difference. And whether you have questions about your current cover, need guidance on policy options, or want to explore a quote, our team is here to help.

Contact our team at he***@******om.au to discuss your options or request a free quote. Let’s work together to secure your business and keep it thriving.

We are incredibly proud to share that two of our senior leaders have been recognised in the Insurance Business Asia-Pacific Elite Women 2026 list, one of the most prestigious acknowledgements of female leadership in the insurance industry across the region.

This year, 70 women across Asia, Australia and New Zealand were named from a field of nominees assessed on leadership impact, influence, innovation and commitment to progress. To have two leaders recognised from our organisation is something we don’t take lightly.

A Big Moment for a Small but Mighty Team

We are a collection of businesses spanning insurance, underwriting, SaaS and premium funding and we turned 40 last year. For a team of just over 40 people, having two leaders named on a list of this calibre is, frankly, a big deal. And we’re going to own that.

Rebecca: Driving Strategy and Technical Excellence

Rebecca, our Chief Insurance Officer, has been instrumental in shaping the technical and strategic heart of our business. She brings deep insurance expertise and a forward-thinking approach to everything she touches and her seat on the Women in Insurance board reflects a commitment to the industry that extends well beyond our four walls.

Kate: Building a Culture Designed to Thrive

Kate, our Chief People Officer, joined with a rich background in diversity, equity and inclusion and has been a driving force behind building a workforce that is genuinely designed to thrive. Not by accident but by design.

Transforming the Business from the Inside Out

What makes this recognition particularly meaningful is what it represents about the way these two leaders have worked together. Over the past year, Rebecca and Kate have collaborated to reshape how our organisation operates from the inside out by building the team by design and redesigning team structures, shifting the focus from presence to output, embedding a values-driven culture, and overhauling the systems our people use every day.

The Results Speak for Themselves

The results speak for themselves: employee turnover reduced by 80%.

Read that again. Eighty percent.

In an era where talent retention is one of the greatest challenges facing businesses of every size, that number is extraordinary and it didn’t happen by chance. It happened because two leaders decided that engagement, culture and people-first thinking weren’t soft initiatives. They were a business strategy.

Building the Future of Work

As we look ahead, our focus continues to evolve. We are actively exploring how AI and emerging technologies can be integrated into our workforce ecosystem in ways that support our people to stay engaged, energised and not overwhelmed. The future of work is something we’re building intentionally, not reacting to.

Looking Ahead with Pride

We are proud of Rebecca and Kate. We are proud of the team that surrounds them. And we are proud to be the kind of organisation, at 40 years young, that still has the appetite to do things differently.

Congratulations to all 70 Elite Women recognised across Asia-Pacific this year. You can read the full report via Insurance Business Asia-Pacific.

Cyber risk is one of the most common threats for Australian businesses. It can disrupt operations and cause serious losses.

To help businesses, the Australian Government released the Essential Eight. This is a set of eight practical cybersecurity strategies. They are designed to help businesses get back to trading quickly after a cyber incident.

Essential Eight Cybersecurity Strategies

The Essential Eight encourages businesses to:

1.Keep software up to date: Regularly update your operating systems and applications to close security gaps.

2. Control access: Only allow authorised staff to make important system changes. Remove access when staff leave.

3. Use strong passwords and MFA: Strong passwords plus multi-factor authentication (MFA) add an extra layer of protection.

4. Limit risky programs: Block or restrict applications and macros that are commonly used to spread malware.

5. Back up data often: Make frequent, secure backups. Test them to make sure you can restore data quickly.

6.Protect against phishing and unsafe sites: Reduce risk from malicious emails and dangerous websites.

7.Have a simple response plan: Know what steps to take and who to contact if something goes wrong.

8. Educate your staff: .Use monthly updates from the Essential Eight team to keep staff aware of the latest cyber threats.

Why Cyber Risk Management Matters

Insurers now look closely at cyber risk management when deciding coverage, premiums, and claims for Australian businesses. Businesses that follow frameworks like the Essential Eight are better prepared if a claim occurs.

Demonstrating these controls can also help negotiate stronger coverage or lower premiums.

What You Should Do?

If you’re reviewing your insurance or risk management, now is a good time to consider how the Essential Eight cybersecurity strategies could be implemented in your business. Contact your broker to discuss these controls in detail.

Mary-Anne has been a client of East West Insurance Brokers for 20 years and we have had the privilege to watch her business evolve from when she owned childcare centres and after-school care facilities to her present business, EPEC Education.

Tell us more about your business.

EPEC Education is a Registered Training Organisation that provides accredited training and professional development to those interested in contributing to the Early Childhood Education community.

EPEC’s training covers all aspects of the care of children with special focus on identifying and preventing child abuse.

What inspired you to start your business?

As a former Approved Provider of a range of early childhood services, I was hoping I could make a positive contribution in this space.

As a former University teacher, I believed the combination of both my theoretical and hands-on industry knowledge would make a positive contribution to the industry.

What’s the most rewarding part of running your business?

Supporting educators and other personnel to be more caring and compassionate in their interactions with the children in their care.

What do you wish you knew starting out?

That it takes a long time to develop the fundamentals of a business, and that there is always a solution to 99% of business problems.

What was your biggest challenge, and your solution?

Coming to terms with all the changing technologies. The best way to overcome these challenges is to stay acutely on top of new technologies and all the details of changing legislation.

What’s your favourite success story?

One of my proudest moments from my business journey is staying true to my belief in the importance of inclusive and compassionate care of all children.

What’s your one big goal for your business in the next year?

In accordance with EPEC’s commitment to the early childhood sector, it is starting to make moves into the recruitment sector and aims to develop this as another department of its business in 2026.

Outside of work, what do you enjoy doing?

Exercising on the beach, connecting with nature and recovering from the challenges of the previous week.

What advice would you give to other business owners?

To be successful in business you need to have plenty of strength and courage. Staying the course is about mental toughness and resilience above all else.

Where can people find you to connect or support your business?

For small business owners, work is more than just work. It is your livelihood. So when something unexpected stops you from working, the stress can be huge. This is where strong insurance claims support makes a real difference.

One of our clients in the commercial cleaning industry experienced this when their work vehicle was damaged in an accident. With jobs booked and bills to pay, being off the road was not just inconvenient. It caused real financial pressure.

The client had a Downtime benefit in their insurance policy, also known as business downtime insurance. This benefit is designed to provide income support while a vehicle is being repaired. After the breakdown, the client lodged a claim and received a repair quote that was below their insurance excess. They decided to pay for the repair privately to avoid the excess.

Partway through the repair, the mechanic found more damage. The new quote was now higher than the insurance excess. Because of this, the client chose to have the repair covered by insurance instead.

The insurer approved the repair costs. However, they declined the Downtime benefit. They relied on a policy exclusion because the first repairs had been done privately.

Our role

Our claims team stepped in to provide dedicated insurance claims support during this stressful time. We reviewed the situation and challenged the insurer’s decision. We explained that:

Any reasonable person would have made the same choice

The client acted in good faith and did not try to mislead

The insurer suffered no additional financial loss from the client going ahead with repairs

We kept the client informed at every step. We reassured them and handled the discussions with the insurer so they could focus on running their business. This is an example of strong insurance broker claims advocacy in action.

The outcome

Because of our team’s experience and persistence, the insurer agreed to pay the maximum Downtime benefit under the client’s business downtimeinsurance. The client received the income support they needed during a difficult period. This reduced financial pressure and helped them return to work with confidence.

Key takeaways:

This claim shows why working with an insurance broker matters:

Policy wording is not always final, and insurers must follow a fair claims process

Experienced claims support can challenge insurer decisions

Brokers provide insurance broker claims advocacy in complex situations

You don’t have to navigate claims alone

Insurance is about being there when it counts and we’re proud to stand beside our clients when they need it most.

Artificial Intelligence in business is now part of everyday operations. It helps with admin tasks, data analysis, and customer service. It can also help write messages and emails. AI is a useful tool for saving time and improving efficiency.

For many businesses, using AI is no longer a choice. It is becoming necessary to stay competitive. But every new tool brings new risks, therefore, it is important to understand these risks before relying on AI.

Understanding AI

A simple way to think about AI is to compare it to your home. A robot vacuum or dishwasher can save you time. But they only work well if the space is set up properly. If there are items on the floor, blocked pipes, or the machine is too full, problems can happen.

AI works in the same way.

The more AI is used in your business, the more important it is to control how it is used. You will need to manage what it can access and who is responsible for it.

Without clear rules and controls, businesses may face challenges. Effective AI risk management can help reduce:

Data privacy and confidentiality breaches

Cyber attacks or system failures

Incorrect results or false information

Intellectual property or copyright problems

Legal or regulatory issues

The Role of Business Insurance for AI

From an insurance point of view, protection must keep up with new technology.

Many insurance policies do not clearly cover AI-related problems. This is common when data, cyber risk, or professional advice is involved. Just as you protect your home and contents, you should also protect your business. This means checking your insurance regularly and making sure your coverage matches how your business uses technology, including AI.

Keeping Business Efficient and Protected

AI can make running your business easier and faster. The key is to set it up properly and ensure you have the right protection in place.

If your business is starting to use new technology or is expanding its use of AI, now is the time to talk to your broker. A review of your risk management and insurance cover, including AI risk management strategies will help make sure your protection grows with your business.

When arranging insurance for a commercial property, many owners make a common mistake: using the purchase price as the sum insured.

On the surface, it feels logical. If that’s what you paid for the property, surely that’s what it’s worth? However, the purchase price doesn’t always reflect the actual cost of rebuilding.

Purchase Price vs. Rebuild Value

It’s important to understand the difference between the purchase price and rebuild value when it comes time to insuring your property. Yes, both relate to what your property is worth, but they represent and serve very different things.

Purchase Price

The purchase price of a property represents the total amount paid to acquire it on the market. It’s affected by several factors, which include:

The value of the land.

The property’s location and market demand.

Broader economic conditions at the time of purchase.

None of these is relevant to an insurer if your building is damaged or destroyed. Insurance is about replacing the structure itself, not the land it sits on.

Rebuild Value

The sum insured is generally expected to reflect the full replacement value of the building, which includes:

Demolition and debris removal.

Professional fees (engineers, architects, surveyors).

Current labour and material costs.

Compliance upgrades (to meet today’s building codes).

What’s the difference?

The key difference between purchase price and rebuild value lies in what each represents. The purchase price reflects the property’s market value, including the land, location, and broader economic factors, while the rebuild value focuses solely on the cost to reconstruct the building if it were damaged or destroyed. This includes demolition, debris removal, professional fees, materials, labour, and any upgrades needed to meet current building codes. In short, insurance covers the cost to rebuild, not the market price you paid.

The cost of getting it wrong

If your sum insured is based on the purchase price rather than a professional valuation, you risk being underinsured. And underinsurance doesn’t just affect you in the event of a total loss. It can also reduce your payout even in the case of a partial claim. For example:

A property was purchased for $2 million, but the actual rebuild cost is $3 million

The sum insured is set at $2 million (instead of $3 million).

A fire causes $600,000 worth of damage

Because the building was underinsured by one-third, the insurer may pay only two-thirds of the claim (about $400,000)

This could leave you, the owner, with $200,000 out of pocket expenses even though the damage wasn’t a total loss.

Why professional property valuations matter

Construction costs in Australia have surged in recent years, driven by shortages of materials and skilled labour. Without a proper valuation, it’s easy to underestimate the cost of rebuilding today compared to when you purchased the property. A professional building valuation gives you:

Confidence that your sums insured are accurate

Protection from co-insurance penalties

Peace of mind that your biggest asset is covered correctly

It’s best to arrange a professional building valuation every few years and review your insurance sums annually. That way, your cover keeps pace with any changes to your property, as well as rising rebuild costs and inflation.

Avoid underinsurance with proper valuation

The purchase price reflects market conditions, not rebuilding costs. Having a commercial property is already a significant investment, and underinsurance can create unexpected financial strain during claims. To safeguard your investment, arrange a professional building valuation and review it regularly. That way, your insurance truly reflects today’s replacement costs, not yesterday’s market value.

When it comes to protecting your assets and ensuring the sums are properly accounted for, a Broker would be a huge help. If you want advice or are interested in learning about available options for commercial property coverage, reach out to East West Insurance Brokers today.

When you think of business insurance, you probably imagine it kicking in after a total disaster, like a fire that levels your building or a car that’s completely written off. But what many business and property owners don’t realise is that even if your loss is only partial, being underinsured can leave you with serious financial strain. Shortfalls in coverage can hurt so you need to be prepared before it’s too late.

What Is Underinsurance?

Underinsurance happens when the sum insured on your policy is less than the true replacement or repair cost of your asset. In other words, you’re insured for less than what it would actually cost to rebuild, repair, or replace. It’s surprisingly common especially with the rising construction costs and inflation. So, if you’re not regularly reviewing your cover, this can also leave you underinsured and underprepared.

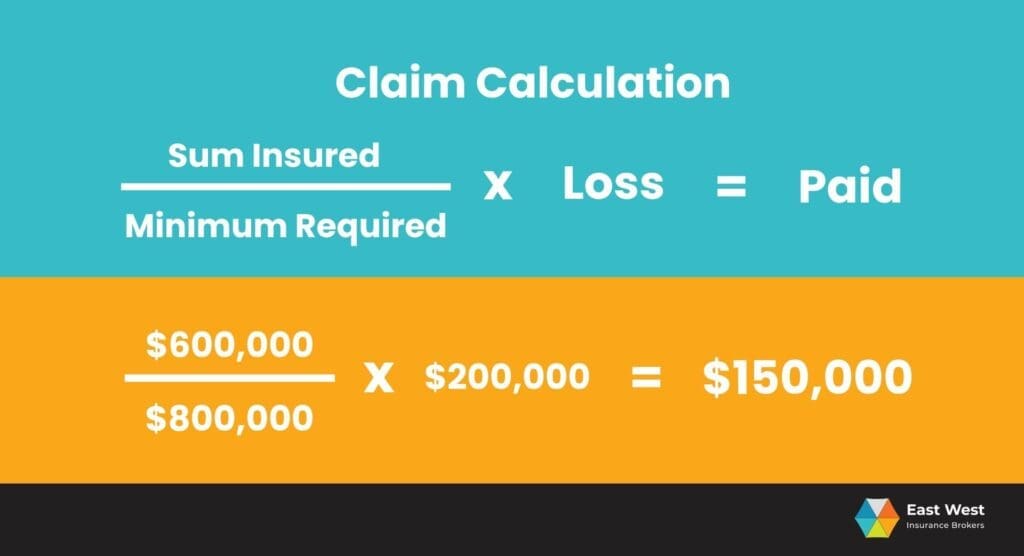

The 80% Co-Insurance Rule in Australia

In Australia, most commercial property and business insurance policies include a co-insurance (or average) clause set at 80% of the asset’s replacement value.

What this means:

If you insure your asset for at least 80% of its true value, the insurer will generally pay the full amount of any loss (up to the sum insured).

If you insure for less than 80%, the insurer can reduce the claim proportionally even if the loss is only partial.

Example:

True Building Value: $1,000,000

Minimum Cover Required (80%): $800,000

Insurance Purchased: $600,000 (60% of true value)

Loss: $200,000

Claim Calculation: (Sum Insured / Minimum Required) X Loss

Example of a claim calculation.

That would be [($600,000 / $800,000) X $200,000] $150,000 paid. Even though the damage was only partial, you’d be $50,000 out of pocket because of underinsurance.

The real-world Impact of underinsurance

Unexpected repair bills – You may have to fund a large portion of repairs yourself.

Cash flow pressure – Reduced payouts can strain your business finances.

Delayed recovery – With less money to repair or replace assets, recovery takes longer.

Business risk – In some cases, underinsurance can threaten not just your return to business, but also your overall ability to keep operating.

How to avoid underinsurance

Get regular valuations – Ensure your building, plant, and equipment values reflect today’s replacement costs.

Factor in inflation – Materials and labour costs rise quickly; your insurance should keep pace.

Review sums insured annually – Don’t just renew “as is” each year.

Work with an Insurance Broker – They understand co-insurance clauses and can explain how it will affect you.

Insurance should offer peace of mind, not unpleasant surprises

You take out insurance for security, not for shock and disappointment. But if your cover is less than 80% of the true replacement value, even a partial loss can leave you with a reduced payout.

So, don’t take the risk. Review your business insurance cover with a Broker. They can even recommend professional valuers to ensure your sums insured are accurate to help you avoid the risk of underinsurance.

If you’d like the support, the team at East West Insurance Brokers is ready to help you perform a review and make sure you’re properly protected.

As Australia moves toward a greener future, the plumbing industry sees a quiet revolution. Environmental regulations are tightening, and more homeowners and businesses are actively seeking sustainable options. For plumbers, this shift presents a golden opportunity that can help them stand out in a competitive market and command premium rates —specialisation in eco-friendly plumbing services

Why Go Green?

Sustainability isn’t just a trend. It’s becoming the new standard as more people turn to greener alternatives. From reducing water waste to lowering energy bills, eco-conscious clients prioritise long-term savings and environmental impact. By positioning yourself as a specialist, you can build trust and long-term relationships with these value-driven customers and get ahead of the game.

Niche areas you can explore

While general plumbing services will always be in demand, specialising can open doors to higher-paying jobs and less competition. Consider niche areas to improve your competitive advantage:

Rainwater tank installations

Given Australia’s variable climate and increasing water restrictions, rainwater harvesting has become more valuable than ever. Installing rainwater tanks for purposes such as garden irrigation, toilet flushing, or laundry usage helps clients reduce their reliance on mains water and lower their water bills.

Greywater systems

Homeowners increasingly seek innovative ways to reuse water from showers, sinks, and laundry. As water conservation becomes more important, there is a growing demand for plumbers who can integrate greywater systems and water-efficient fixtures into homes and businesses. Greywater systems provide an eco-friendly solution that helps households reduce their water usage. By specialising in installing and maintaining these systems, you position yourself as a forward-thinking plumber who can offer both environmental and economic benefits while ensuring compliance with local council regulations.

Energy-efficient systems

With rising energy costs and sustainability at the forefront of Australians’ minds, more Australians are investing in energy-efficient hot water systems. Solar hot water, heat pump systems, and instantaneous gas units are all in high demand. By becoming an expert in these technologies, you can offer high-value services backed by federal and state incentives, making your offerings more attractive and financially accessible to clients.

Backflow prevention testing

To protect drinking water supplies, backflow prevention devices are legally required in many commercial and industrial settings. Certified plumbers who offer testing, maintenance, and compliance reporting can secure ongoing contracts with commercial clients. This niche provides a reliable, repeat-business stream and sets you apart as a compliance-focused professional.

Thermostatic Mixing Valve (TMV) Servicing

TMVs are critical in healthcare and hospitality settings to ensure safe water temperatures. Regular inspection and maintenance are required to meet safety standards. Specialising in TMV servicing provides access to a regulated market with potential for more repeat business.

Drainage & pipe relining

Compared to traditional pipe replacement, pipe relining offers a cost-effective, no-dig solution. Investing in modern equipment and training allows you to provide efficient solutions for blocked or damaged drains, appealing to homeowners and businesses.

Gas fitting services

Gas fitting is a consistently in-demand service in Australia and with proper licensing, you can handle various jobs from appliance installations to leak detection. Expanding into gas work can massively increase your earnings and service offerings.

The business advantage for sole traders

Specialisation means more than just offering a service—it’s about becoming known for it. When you focus on one or two key areas, marketing becomes easier, and referrals come faster. Plus, clients are often willing to pay more for someone with proven expertise in the solution they need You also reduce price-based competition, improve efficiency through repeated processes, and gain more profound knowledge in your chosen field—all of which help your bottom line.

Ready to Make the Shift?

If you’re thinking about expanding your plumbing business, consider how you can incorporate eco-friendly plumbing solutions into your service offering. Start with the systems you’re already familiar with, then upskill and work to get certifications to build credibility. As demand grows and sustainability becomes the norm, those who specialise early will be in a prime position to grow their business and make a lasting impact. Being an Australian sole trader plumber can be challenging at times, but it also offers incredible freedom and direct rewards. As your own boss, you have the flexibility to set your own hours, within certain limits. However, this also means that the success of your business is closely linked to your hard work and skills. To continue thriving in the plumbing industry, it’s important to embrace opportunities and invest in yourself.

Protect your business with tailored commercial property insurance from our Australian experts. Over 40 years of experience. Get your free quote today!

What do a cozy cafe, a small retail shop, and a towering office building have in common? They all face similar risks when it comes to protecting their property. From fires and floods to theft and vandalism, these unexpected events can disrupt operations—or even force a business to shut down entirely.

That’s why having appropriate commercial property insurance is important. Whether you own or lease your space, your insurance can be the lifeline safeguarding your business from financial fallout.

But before you start insurance shopping, you should first get your commercial property professionally valued.

What is a property valuation?

The estimated market value of a property, which a qualified professional appraiser usually performs. This assessment is based on various factors, which include:

Condition of the property

Existing structures

Location and proximity to other facilities

Market trends

Renovations and upgrades

Size and layout

Valuation of similar properties within the area

There are two main types of property valuations, each serving different purposes. Understanding the distinction between them is crucial to avoid costly mistakes.

Real estate valuation – Used for buying, selling, or securing a mortgage. This type of valuation assesses a property’s sale value, which is influenced by current market trends.

Insurance valuation – Used in insurance applications. It focuses on the cost of rebuilding or repairing a property based on current construction costs.

Insurance valuations are sometimes calculated using a $ per square metre estimate. However, general property valuers may not be qualified to quote rebuild costs. To ensure you’re not underinsured, it’s recommended to consult a surveyor for a more accurate figure.

It’s also important to remember that real estate and insurance valuations can differ significantly, sometimes in millions, and should not be used interchangeably.

How can property valuation impact insurance?

Insurers may use the property valuation report to determine what coverage is necessary and calculate the total cost of the premiums they’ll offer. A higher property value can mean more payouts are required in the event of a repair or replacement claim, leading to higher premiums. On the other hand, they may offer lower premiums to properties with lower value. The catch is this may mean less coverage and more out-of-pocket costs in case of a claim.

You need an accurate property valuation to balance adequate coverage and manageable premiums. This would help you avoid the following:

Over-insuring

Securing as much coverage as possible may sound like the safer option. However, insurers typically don’t pay more than the actual repair cost or the property’s market value. If your property is overvalued, this might lead to over-insuring and paying higher premiums for coverage you may not even need.

Underinsuring

Undervaluing your commercial property to pay lower premiums may sound like an easy way to save money, but it won’t help your business long-term. You may end up exposed to the risk of being underinsured in the event of a claim. Payouts from insurers may not cover enough repair or replacement costs, leading to additional financial strain.

Penalty fees

Policies may include a ‘co-insurance’ clause, which requires the property to be insured to a certain percentage of its value. If your property is found to have been undervalued, your insurance company may penalise you with a penalty fee or reduce the payout in the event of a claim.

Legal issues

An inaccurate commercial property valuation may also violate contractual agreements for leasing and mortgage.

It’s advisable to have your property professionally revalued every few years or whenever significant changes occur, such as renovations, expansions, or shifts in the local market. This helps you and your insurance provider update your coverage to match your business needs.

Having accurate and up-to-date valuation also minimises disputes during claims because insurers are better equipped to assess losses accurately, ensuring a smoother claims process.

Secure your commercial property

Having an accurate and up-to-date property valuation empowers you to make smart financial decisions while ensuring you have adequate insurance coverage to protect your investment. In business, preparation is everything—and staying ahead begins with understanding the true value of what you own.

Want to learn more about commercial property insurance? Connect with East West Insurance Brokers! Our team of expert insurance brokers can provide valuable insights into commercial property coverage for you and your business. Contact us today to get started!

The future of the global welding industry looks bright. As demand from sectors like automotive, construction, and heavy engineering continues to rise, the industry’s value is projected to grow from USD 24.73 billion in 2023 to USD 34.18 billion by 2030. Australia is poised to be a key player in this exciting transformation. But what developments are in store for the welding industry?

Increasing Demand for Skilled Welders

“By 2030, we will be 70,000 welders short“, according to Geoff Crittenden, chief executive of Weld Australia. It’s an issue faced by other countries, such as the United States and Japan.

While the worker shortage can mean more employment opportunities for aspiring welders, given the numerous ongoing infrastructure and expansion projects, there is a pressing need to address it now. As a result, the Australian government is encouraging more investment in the welding industry by funding businesses and nurturing the talent pool through various programs.

Promoting Diversity in Trades

Women make up 48% of the country’s workforce. However, less than 1% in the welding and fabrication sector are women. Part of addressing the worker shortage is taking a proactive approach to promoting opportunities for women. In 2022, the Victoria government launched the Building Equality Policy to support women in getting into male-dominated industries. More projects are also being funded to encourage other underrepresented groups to enter trades and STEM training.

Skilled Migration Program

Australia is also looking to address the labour shortage with the Skilled Migration Program, which reopened in October 2023 with new criteria. The government has streamlined the visa process to help experienced and skilled tradespeople from overseas apply for jobs in Australia. This helps fill vacant positions and fosters regional development by introducing global talents.

Innovation Through Technological Advancements

As demand grows, technology advances to cope, and the welding industry is no exception. The launch of Industry 4.0 last year has given a boost by pushing for the integration of digital technologies like AI, Internet of Things (IoT), and robotics. These have dramatically enhanced productivity while supporting Australia’s sustainability efforts by promoting energy-efficient practices. Here are just some examples:

3D printing – Allows for the rapid creation of prototypes and complex components, unlocking new design possibilities while minimising waste during the design phase.

Internet of Things (IoT) – Utilises real-time data reporting to enable predictive maintenance, helping reduce downtime and enhancing operational efficiency during critical issues.

Robotic and laser welding – Transforms traditional welding practices by enhancing precision and quality, creating new opportunities for businesses to optimise and deliver superior results.

Switching to Renewable Energy

35% of the total electricity generated in Australia last year was from renewable energy sources. It’s only expected to rise in the following years as the country ramps up efforts to transition to greener energy sources as part of the nationwide goal of reaching net-zero carbon emissions by 2050. Multiple legislation and projects have been introduced to boost support.

Capacity Investment Scheme

First introduced in December 2022 and then expanded in November 2023, the Capacity Investment Scheme aims to unlock $40 billion in private investment into the local manufacturing industry to create more jobs and improve local economic participation in the renewable energy transition.

Future Made in Australia Act

One such effort is the Future Made in Australia Act, a major piece of legislation passed in 2021. Under this, the Australian government commits to providing funding and incentives for businesses to invest in manufacturing capabilities and to adopt cleaner technologies. It aims to make the country’s economy more sustainable, increasing the resilience of supply chains and boosting the manufacturing industry’s ability to compete globally.

State Prosperity Project

The South Australian Government also launched the State Prosperity Project early this year to reindustrialise the Upper Spencer Gulf by harnessing its mineral resources, renewable energy, and green manufacturing potential. The project is in partnership with education and training providers like the Technical College in Port Augusta, opening in 2025. This college will adopt a part-time operation model, offering industry training and work opportunities across the region.

Evolve with the Welding Industry

As the welding market evolves and unveils new opportunities for innovation, you need to continue learning and enhancing your skill set. Stay alert to new trends so you can embrace them and secure a stronger competitive edge. You also need to be aware of any potential risks you’ll face in the industry.

Safeguard your journey with East West Insurance Brokers. Our team of insurance experts will guide you through your insurance options, empowering you to make informed decisions to protect your business.

Visit our website today to request a quote so you can confidently forge ahead!

Retail businesses face more unique challenges today when it comes to security. Threats are not only limited to physical damages and losses. With more people relying on digital transactions, online threats are ever-changing and can even be more damaging.

In this blog, we’ll discuss security strategies you can implement to safeguard your retail business. From offline to online, we’ve got you covered!

A well-designed store layout can do wonders for business growth. Customer experience can be improved by making it easier to find things they might like or need. You can boost sales by highlighting marketable or high-priced items. It can also improve your store’s security by deterring theft and intruders.

A good theft prevention strategy is reducing blind spots would-be thieves could exploit. You can do this by strategically placing shelves and installing mirrors between the aisles. This makes it easier for store employees to monitor customers and send alerts in case of emergencies. It’s also recommended to place higher-priced products near where employees can keep a close watch, preferably far from any exits.

Install surveillance and alarm systems

Ensuring complete visibility within a store is hard, and employees can’t keep an eye on everything at all times, so integrate surveillance and alarm systems in your store. Install security cameras near any entrances or exits, parking areas, and cashier stations. You can prop them up so they’re more visible and act as a deterrent. However, the more visible your cameras are, the easier they can be to avoid or destroy during a break-in.

For additional security, consider installing motion detectors with lights and alert systems to scare off potential intruders. Installing glass break sensors for windows and displays is also recommended.

Control access

Limit access to areas like stockrooms, offices, and surveillance rooms. Most stores have passcodes which can be easy to set up but also be easy to bypass. To enhance your store security, consider implementing key card systems or biometric scanners with secure locks to effectively control access and ensure that only authorised personnel can enter these areas.

Cybersecurity

Protect sensitive digital information with data encryption

As a retail business, customers often share sensitive information like their names, addresses, phone numbers, and credit card details. If this information falls into the wrong hands, it could damage your business and pose a threat to your customers’ personal security. Improve your digital security by implementing end-to-end data encryption.

Provide secure payment processing

One of the most common times that’s prone to data theft is during payment processing for digital wallets and cards. Vet third-party payment vendors. Perform comprehensive research on their background and customer feedback.

Perform checks and updates regularly

Don’t be complacent after installing cybersecurity measures. Stay vigilant and frequently check every software or security system to ensure it’s always up to date. This will help you detect abnormal activities, malware, and potential security breaches.

Employee Training

Train for identifying and preventing theft

Your employees are your greatest asset and, with proper training, can be very helpful in improving store security. Encourage vigilance and regular checks. Provide training on identifying suspicious behaviour, learning theft prevention strategies, and implementing store security policies.

Cyber threats can also target your employees so it’s important to provide comprehensive training on how to handle sensitive information, including customer data and payment details.

Perform regular audits

Besides regularly performing cybersecurity checks, it’s also important to perform regular audits on your store’s physical inventory. This helps ensure accurate stock levels and identify discrepancies early. Regular inventory checks are also a good theft prevention strategy by encouraging employees to be accountable.

Insurance

General Liability Insurance

Having General Liability Insurance provides added financial security by protecting your business against claims of personal injuries, property damage, or loss within store premises. For example, if a customer is pickpocketed inside your store or injured in the parking lot and then accuses the store of negligence, General Liability Insurance may help cover repair and legal costs.

Commercial Property Insurance

Commercial Property Insurance, like General Liability, can cover repair and legal costs. The difference is that it can provide coverage for losses directly suffered by the store from incidents like property damage, inventory theft, and equipment breakdown.

There are many factors and risks that you need to consider, so it’s best to speak with an insurance broker. You can contact East West Insurance Brokers to submit an inquiry and receive more information.

Business Interruption Insurance

Unforeseen circumstances and emergencies can cause significant financial damage to retail businesses, so Business Interruption Insurance is necessary. Depending on the coverage you include, it can cover loss of income, ongoing expenses during repairs, and even temporary relocation costs.

Secure your retail business with appropriate coverage

Want to find appropriate coverage for retail business insurance but don’t know where to start? Our East West Insurance Brokers team is ready to help you explore your options to protect your business. Get in touch and secure your future with us today!

The business world can be unpredictable, and even minor events can disrupt daily operations and affect your profits. That’s why having Business Interruption Insurance is critical to a solid risk management strategy. But what is Business Interruption Insurance, and how can you ensure you have the appropriate coverage for your business’s needs?

Business Interruption Insurance covers lost business income or profits and operating expenses when the business cannot operate as usual. Incidents may include natural disasters and when a facility or equipment sustains damage. However, Business Interruption Insurance works differently from Property and Equipment Insurance. Rather than providing cover for property repair or replacement costs, business interruption aims to cover the loss of income to the business due to the damage sustained or equipment breakdown.

Examples of Benefits and Coverage

Various benefits and specialised coverage areas are needed to maintain financial stability and reduce the damage caused by disruption to business operations. Here are some common examples of the benefits and what the insurance typically covers:

Income loss (calculated based on previous financial statements)

Operating expenses (utility bills, property rent, other fixed costs)

Employee wages (may include benefits and training costs)

Tax and loan payments

Additional expenses (relocation, equipment repair or rental)

Specific exclusions and constraints can be added to the insurance policies that you must watch out for. It’s ideal to routinely review coverage details to avoid surprises when an incident occurs. You also need to check for other coverage that may be required depending on the nature of your business and service. Contact East West Insurance Brokers to explore your options and find the insurance that suits your business.

Common Mistakes and How to Avoid Them

Underestimating coverage needs and costs

A common oversight many business owners make is underestimating the full impact of operational interruptions and focusing solely on lost revenue. When evaluating Business Interruption Insurance, consider the entire spectrum of operational costs, from daily expenses, employee wages and benefits to supply-related expenditures.

Where your business is located and what type of industry you’re in plays a vital role in determining the necessary coverage and premium costs. Those operating in high-risk areas and industries require even more comprehensive coverage. Properly assessing these elements when selecting your policy helps ensure your business remains resilient despite unexpected challenges.

Failing to review and update insurance policy terms and conditions

Business Interruption Insurance policies vary regarding coverage, limits, and exclusions. Before signing the dotted line, it’s essential to review the insurance policy terms and conditions to ensure it meets your business’s specific needs. Pay close attention to factors such as the waiting period before coverage kicks in, the length of coverage, benefit period, and any limitations on coverage for specific events.

Remember to review current insurance coverage regularly after signing, too. Always take a proactive approach and stay informed about your policy details. It can help you identify any necessary updates or adjustments as your business grows and evolves.

Not considering additional or specialised coverage

Each business is unique, with specific challenges and requirements shaped by its industry, location, and operational scope. Part of a good risk management strategy should be evaluating the additional or specialised coverage and integrating custom insurance solutions. So, consider the following:

Prevention of Access (PA)

Many unforeseen events can disrupt business operations, from natural disasters to other dangerous situations. These may prevent you from operating your business and even restrict access to your premises by a legal authority ordering the evacuation of the public. This is where Prevention of Access comes in. It’s a specialised type of coverage under Business Interruption Insurance that protects against loss resulting from interruption of, or interference with, your business as a result of damage or threat of damage to property in the vicinity of the premises covered by the policy.

Suppliers and/or Customers Premises (SCP)

SCP is a specialised type of coverage that aims to protect businesses from financial losses resulting from property damage or loss at specified suppliers’ or customers’ premises. Suppose a manufacturing company faces significant delays and income loss due to a key supplier’s failure to deliver the necessary components in production following an insured event at their location, SCP can help mitigate the loss. On the other end of the supply chain, if your business relies on revenue from major customers who cannot complete their purchases due to property damage at their own premises, you can file a claim to minimise your losses.

Public Utilities Extension (PUE)

While SCP protects against issues with third-party businesses in the supply chain, PUE is related to utility providers. It mitigates financial instability when utility services fail and disrupt normal operations as a consequence of damage to any land-based property anywhere in Australia or New Zealand. This includes incidents involving any utility company producing, transmitting, supplying or delivering electricity, gas, water, sewerage or communication products or services used by the business. Companies in manufacturing, hospitality, and IT can significantly benefit from PUE.

Inaccurate or improper documentation

If you’re filing an insurance claim for loss of revenue, proper documentation is critical to ensuring that you receive the full benefits of your Business Interruption Insurance policy. Keeping detailed records of your finances and any communication with your insurance provider also reduces the likelihood of being denied.

Seek advice from a professional

Avoid making these common mistakes. Discover how to calculate your Business Interruption Insurance and get a reliable estimate. Seek advice from a professional insurance broker to ensure your business is covered as effectively as possible.

East West Insurance Brokers can assist you in evaluating your business’s requirements and comparing coverage options from multiple providers. Our team of experienced Insurance Advisors will provide valuable insight as you navigate different policies’ various terms and conditions. Get in touch with us today and get insured.

Starting a new business can be an exciting and challenging endeavor but as a new business owner in Australia, you will have many things to consider, including finding business insurance with suitable coverage. To help you on your journey, we have compiled a checklist of coverage based on your general business needs and how insurance can protect your business.

We live in a digital age with growing cyber threats. So Cyber Liability Insurance is becoming increasingly important, especially for businesses that store sensitive customer data or rely on technology and online platforms for their operations. The level of security may differ, but generally, Cyber Liability Insurance provides coverage for data breaches, cyber-attacks, and other online threats like hacking or data theft that can impact your business.

Public Liability Insurance

If your business interacts with or works with the public, one major insurance you’ll need is Public Liability Insurance. It provides coverage for claims against your business from property damage or third-party personal injury caused by your operations. This can be from activities at the workplace or at another location. Public liability insurance helps protect you from potential lawsuits.

Product Liability Insurance

Similar to Public Liability Insurance, product liability provides coverage for claims of property damage or third-party personal injury. The difference is instead of being a result of operations, product liability covers claims made against the products you sell or supply.

Professional Indemnity Insurance

When you provide services or advice to customers, Professional Indemnity Insurance protects your business from claims of negligence or errors and omissions in your services.

Insurance for Properties and Assets

Commercial Property Insurance

Whether small or big business, Commercial Property Insurance is essential regardless of your industry. It covers any properties or assets used for your business operations, including infrastructure, equipment, and inventory against damage or loss due to fire, theft, vandalism, or natural disasters.

Investing in property insurance is not just about compliance or managing risk but also about ensuring the continuity and resilience of your business. By protecting your physical assets, you can mitigate the impact of unforeseen events, keeping your operations running smoothly and speeding up recovery after adverse situations.

Equipment Breakdown Insurance

You’ll want Equipment Breakdown Insurance if your business relies on machines or technological equipment. This is not typically included in standard Commercial Property Insurance but is essential for businesses in manufacturing, technology, restaurants, and any other niche that heavily depends on functional equipment.

Equipment Breakdown Insurance can cover the repair or replacement costs of equipment that breaks down unexpectedly due to causes like motor burnout, power surges, or mechanical malfunctions. Beyond covering physical damage, it often addresses business losses incurred from equipment downtime, such as lost income and extra expenses needed to expedite repairs or procure temporary replacements.

Flood Insurance

Flood Insurance may only sometimes be included in Commercial Property Insurance. However, it is still a must-have, mainly if you operate in areas prone to flooding or work in an industry where the threat of flooding can derail business operations.

Finance Insurance

Business Interruption Insurance

When business operations are disrupted, whether by fire or weather conditions, Business Interruption Insurance can help you remain financially stable by covering the loss of income and even unforeseen expenses.

Credit Insurance

Credit Insurance is a risk management tool that helps businesses protect themselves from potential losses if their customers are unable to pay their debts. It’s particularly useful for businesses offering credit to customers, providing confidence when entering new markets or dealing with larger accounts. This insurance also helps companies manage credit risk effectively and optimize credit and collection procedures, safeguarding their financial health.

Workers’ Compensation Insurance

Workers’ Compensation Insurance is a mandatory insurance policy for businesses in Australia aimed at protecting employees if they become ill or injured due to their work. This type of insurance provides coverage for wages lost during the time off work, medical expenses, and rehabilitation costs needed to help the worker return to work.

The requirements and implementation of Workers’ Compensation Insurance can vary considerably across different states and territories in Australia. Differing regulatory bodies also manage worker’s compensation schemes. The State Insurance Regulatory Authority (SIRA) regulates those based in New South Wales, but WorkSafe Victoria manages insurance in Victoria.

So, before you work on finding business insurance for Workers’ Compensation, check your local regulatory office to ensure compliance.

Get your business insured

Finding business insurance doesn’t have to be complicated or stressful. At East West Insurance Brokers, we specialise in simplifying the process, helping you find the insurance coverage that best fits your business needs. Whether you’re just starting or looking to enhance your current policies, our team of dedicated Insurance Advisors is here to guide you every step of the way.

Don’t let uncertainties slow you or your business down. We’re here to help you secure your business’s future. Contact us today and get insured.

Getting business insurance is essential, but the first step of obtaining a business insurance quote can be very demanding. This process requires you to provide extensive information about your business, not only for assessing and understanding the potential risks your business may face but also for determining the most effective protection strategies and estimating the overall cost of business insurance. But what exactly is required to get an accurate insurance quote?

Provide detailed information about your business to make it easier to assess the level of risk associated with insuring your business and affects the total cost of business insurance. This generally includes the following:

Business Name: The legal name of your business.

Business Address: The physical location of your business.

Industry Type: The industry or sector in which your business operates.

Number of Employees: The total number of employees working for your business.

Annual Revenue: The yearly income generated by your business.

Previous Insurance Coverage: Details of your business’s previous insurance coverage (if any).

2. Assets and Inventory

Another essential piece of information you need to provide is a comprehensive list of current assets and inventory. This should include specifics about the property where your business operates, the equipment utilised in daily operations, and any other assets requiring insurance coverage. The total value of your assets is factored in the calculation of your business insurance quote and can affect what coverage is recommended which leads to the next thing that needs to be assessed.

3. Coverage Needs

Clearly outline your coverage needs when you’re looking for a business insurance quote. By understanding and clearly expressing the specific protections your business requires, you help your insurance provider create a quote that matches your business’s unique needs. This careful preparation not only leads to a more accurate assessment but also ensures that you get the best and most comprehensive coverage.

Here are some examples:

General Liability Insurance – protection against claims of bodily injury or property damage to third parties resulting from business operations.

Property Insurance – covers damage to business property and assets due to events such as fire, theft, vandalism, or natural disasters.

Cyber Liability Insurance – with the increasing threat of cyberattacks and data breaches, businesses need coverage to protect against losses due to hacking, data theft, or other cyber incidents.

Commercial Auto Insurance – if your business owns vehicles or if employees use their vehicles for work purposes, this insurance provides coverage for accidents, injuries, and property damage involving those vehicles. This can be especially useful if employees often travel for work events.

Product Liability Insurance – for businesses that manufacture or sell products, this coverage protects against claims of injury or damage caused by defects in those products.

If you need clarification on what other types of coverage your business will need, contact East West Insurance Brokers. We are here to help you assess your requirements and needs to find the best coverage plan.

4. Claims History

Be ready to provide detailed information about any past insurance claims your business has filed, including the nature of the claims and the amounts paid out. Your business’s claims history is a significant factor in determining the cost of your insurance premiums.

Insurance providers use this history to gauge the risk level of insuring your business. A track record of frequent or high-value claims might indicate higher risk, which could lead to increased premium costs. Accurate and comprehensive details about your claims history help the insurance company provide a fair assessment and pricing for your coverage.

5. Risk Assessment

Factors such as your industry, business operations, location, and safety measures are pivotal in the risk assessment process. Providing detailed and accurate information about these aspects will help ensure that your insurance quote is accurate and tailored to your needs. Many insurance providers include risk assessment services with their policies, offering a convenient option for assessing your business risks. Alternatively, hiring a specialized risk management consultant can provide a more in-depth analysis tailored to your specific industry or business niche.

Conducting your own risk assessment is another viable strategy. Start by identifying potential hazards, vulnerabilities, and threats that could impact your business operations. Also consider external factors from economic conditions, local and global politics, as well as health and environmental issues.

Staying informed through industry publications and news sources is crucial for anticipating and mitigating future risks. There are multiple online resources available to assist businesses in conducting self-assessments and pinpointing potential risks. Being proactive can empower you to better manage and analyse your business’s vulnerabilities.

Looking for a convenient way to get a business insurance quote?

Conducting your own risk assessment to get an estimate cost of business insurance can be time-consuming, particularly when your priority is managing day-to-day business operations. At East West Insurance Brokers, we understand the importance of your time and the complexities of navigating multiple insurance policies. Our team is dedicated to guiding you through the process and identifying the coverage that best suits your needs. Contact our team today to streamline your insurance process and ensure your business is protected.

Agriculture is a cornerstone of Australia’s economy and food security. The industry, however, is vulnerable to climate change, soil degradation, and water scarcity. Weather, pest outbreaks, and market fluctuations also threaten farmers’ financial security. That’s why it’s recommended that farmers get agriculture insurance for financial protection and stability amid environmental uncertainties.

Whether you’re a small-scale farmer or part of a large agricultural operation, considering agriculture insurance is a wise decision, and East West Insurance Brokers is here to help. Our team of expert Insurance Advisers can help you navigate the insurance market and shop around for a good coverage plan. Contact us today to stay protected.

Government agencies and nonprofit organisations alike have implemented initiatives to enhance agricultural productivity while preserving natural resources. Let’s explore a few of these programs and initiatives driving sustainable agriculture in Australia.

Australia’s Net Zero Plan is a bold and ambitious initiative to reduce carbon emissions by 43% by 2030 and achieve net zero emissions by 2050. The plan seeks to achieve these goals through the support of independent and nonprofit organisations, to create a more sustainable and environmentally friendly future for Australia.

But how does this affect the agricultural sector?

Well, the agriculture industry plays a significant role in greenhouse gas emissions (GHG), mainly through livestock production, fertiliser use, and land use changes. They account for 15% of the total emissions in 2019. Meeting net zero targets will require substantial changes in farming practices, potentially impacting productivity, profitability, and livelihoods. Here are the common practices that are being adopted today:

Acceleration of the transition to renewable energy

Planting cover crops to improve soil quality and prevent erosion

Improving fuel efficiency of fishing vessels

Investing in new technology to increase efficiency and reduce waste or raw material consumption

For their part, the Australian Government is developing plans to provide farmers with the necessary education and support to reduce GHG emissions.

Climate-Smart Agriculture Program

The Australian Government established the $300 million Climate-Smart Agriculture Program through the Natural Heritage Trust (NHT). Below is a sample of programs they offer grants to farmers:

Partnerships and Innovation Grants

The program offers grants ranging from $250,000 to $5,000,000 for medium to large-scale projects that promote climate-smart agriculture practices. The application for the first round began on 22 February 2024, and the second round is still being discussed.

Small Grants

Another grant is offered for projects focused on increasing on-farm productivity and sustainable agriculture for community groups. The start date for application is to be announced later this year.

Soil Capacity Building

The Australian Government has invested $21 million in a program that monitors soil quality nationwide. This program aims to gather and assess data about soil trends. Additionally, $6 million has been invested in improving the sharing and use of soil data through the Australian National Information System.

NFF 2030 Roadmap

The National Farmers’ Federation (NFF) spearheaded the development of the NFF 2030 Roadmap, which was developed through a collaborative process that involved more than 300 representatives in the agricultural sector. Created as a strategic blueprint, the 2030 Roadmap identifies key opportunities and challenges in the agricultural sector. Essentially, it’s developed as a guide for growth and sustainability.

The NFF releases annual reports to track progress, maintain accountability, and push continuous innovation for everyone involved. You can access the 2030 Roadmap and its annual reports here.

Australian Agricultural Sustainability Framework

Another initiative by the NFF, with the support of the Australian Government, is the Australian Agricultural Sustainability Framework (AASF). It aims to promote responsible environmental stewardship by upholding ethical practices in compliance with the law, reducing GHG emissions, and preserving the environment. The framework also encourages the development of communities by nurturing the well-being of people and animals.

The AASF started in 2020 and is still in ongoing development. However, you can visit their site to learn more about the initiative.

FutureFeed

Farming, particularly livestock, is a major methane emitter and GHG contributor in Australia. As a solution, the Commonwealth Scientific and Industrial Research Organisation (CSIRO) established the FutureFeed program.

It aims to reduce GHG emissions, boost animal health, and improve farm efficiency with the development of a sustainable feed supplement for livestock using Asparagopsis seaweed.

FutureFeed currently provides licenses for growers and processors rather than selling seaweed directly. If you want to buy the product for your livestock, you can buy from their licensed seaweed growers.

The Future of Sustainable Agriculture

Challenges and triumphs, emphasising innovation, adaptation, and collective action, mark Australia’s journey toward achieving net zero carbon emissions by 2030. The goal, however, extends beyond meeting the deadline. It sets the stage for a sustainable future that preserves Australia’s diverse environment while pushing for innovation and collaboration across all industries. Australia is also contributing to the global fight against climate change for a greener future by adopting transformative technologies and forming eco-partnerships.

The field of civil engineering is challenging and requires hard work, dedication, and adaptability as technology continues to advance. And if you’re looking to improve your chances of success as a civil engineer, here are some practical tips that can help you stand out:

Civil engineering is constantly evolving and adapting to new technologies and methodologies. Stay ahead by expanding your knowledge. Focus on enhancing your abilities by mastering software programs like AutoCAD or gaining expertise in structural analysis. Seek diverse projects that challenge your skills and ask experienced professionals for guidance. You can also try the following:

Attend workshops and trainings

Explore online programs and resources

Subscribe to industry newsletters or set up alerts to receive news directly to your email

These will help you keep up with the latest industry trends and make you more valuable to employers and clients.

Learning and mastering new technologies can be exciting, especially in civil engineering, where new technologies are developed daily. However, keep in mind that while using new technologies may impress your clients or team, it’s essential to ensure that all the platforms you use are compatible to avoid any future issues. It would be frustrating to spend a lot of time working on a project on one platform only to find that you cannot access it on another.

So before you jump into working on any project and introducing a new software or tool, ask the following questions: