When you think of business insurance, you probably imagine it kicking in after a total disaster, like a fire that levels your building or a car that’s completely written off. But what many business and property owners don’t realise is that even if your loss is only partial, being underinsured can leave you with serious financial strain. Shortfalls in coverage can hurt so you need to be prepared before it’s too late.

What Is Underinsurance?

Underinsurance happens when the sum insured on your policy is less than the true replacement or repair cost of your asset. In other words, you’re insured for less than what it would actually cost to rebuild, repair, or replace. It’s surprisingly common especially with the rising construction costs and inflation. So, if you’re not regularly reviewing your cover, this can also leave you underinsured and underprepared.

The 80% Co-Insurance Rule in Australia

In Australia, most commercial property and business insurance policies include a co-insurance (or average) clause set at 80% of the asset’s replacement value.

What this means:

- If you insure your asset for at least 80% of its true value, the insurer will generally pay the full amount of any loss (up to the sum insured).

- If you insure for less than 80%, the insurer can reduce the claim proportionally even if the loss is only partial.

Example:

- True Building Value: $1,000,000

- Minimum Cover Required (80%): $800,000

- Insurance Purchased: $600,000 (60% of true value)

- Loss: $200,000

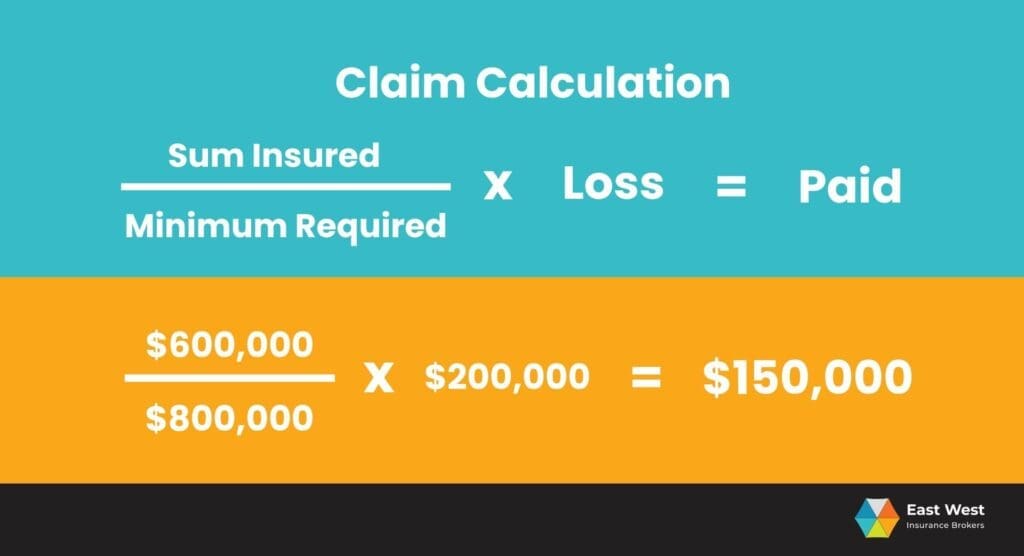

- Claim Calculation: (Sum Insured / Minimum Required) X Loss

That would be [($600,000 / $800,000) X $200,000] $150,000 paid. Even though the damage was only partial, you’d be $50,000 out of pocket because of underinsurance.

The real-world Impact of underinsurance

- Unexpected repair bills – You may have to fund a large portion of repairs yourself.

- Cash flow pressure – Reduced payouts can strain your business finances.

- Delayed recovery – With less money to repair or replace assets, recovery takes longer.

- Business risk – In some cases, underinsurance can threaten not just your return to business, but also your overall ability to keep operating.

How to avoid underinsurance

- Get regular valuations – Ensure your building, plant, and equipment values reflect today’s replacement costs.

- Factor in inflation – Materials and labour costs rise quickly; your insurance should keep pace.

- Review sums insured annually – Don’t just renew “as is” each year.

- Work with an Insurance Broker – They understand co-insurance clauses and can explain how it will affect you.

Insurance should offer peace of mind, not unpleasant surprises

You take out insurance for security, not for shock and disappointment. But if your cover is less than 80% of the true replacement value, even a partial loss can leave you with a reduced payout.

So, don’t take the risk. Review your business insurance cover with a Broker. They can even recommend professional valuers to ensure your sums insured are accurate to help you avoid the risk of underinsurance.

If you’d like the support, the team at East West Insurance Brokers is ready to help you perform a review and make sure you’re properly protected.